The KCCU Blog

Back-to-school season is an exciting time, but it can also put a strain on your family's budget. Between school supplies, clothing, extracurricular fees, and technology needs, expenses can add up quickly. The good news? A little planning can help you stay on budget while still making sure your child is ready for a successful school year.

Here are some simple budgeting hacks to help stretch your dollars this back-to-school season.

1. Start With What You Already Have

Before heading to the store, take inventory of last year's supplies. You may already have notebooks, folders, pencils, calculators, backpacks, or lunch containers that are still in great condition. Reusing items not only saves money but also reduces waste.

2. Make a List - and Stick to It

Schools often provide supply lists before classes begin. Use that list as your guide and avoid impulse purchases. Shopping with a plan helps prevent overspending on items your child may not actually need.

3. Set a Spending Limit

Determine how much you can comfortably spend before you shop. Consider creating a budget for categories like:

- School supplies

- Clothing and shoes

- Lunch essentials

- Sports or activity fees

- Technology or accessories

Having a clear spending limit helps you prioritize purchases and avoid surprise expenses

4. Shop Sales and Compare Prices

Back-to-school sales can offer significant savings, but not every "sale" is the best deal. Compare prices between local stores and online retailers before making purchases. Shopping early can also help you find better selection and avoid paying premium prices closer to the start of school.

5. Buy Only What You Need

It can be tempting to purchase every trendy notebook, water bottle, or backpack on the shelf. Focus on necessities first. If your budget allows later in the year, you can always add fun extras as rewards or gifts.

6. Take Advantage of Tax-Free Shopping Events

If your state offers a sales tax holiday for back-to-school purchases, plan your shopping around those dates whenever possible. Saving even a small percentage on larger purchases can make a noticeable difference.

7. Spread Out Larger Purchases

If your child needs a laptop, graphing calculator, or other expensive item, consider purchasing it separately from your regular school shopping. Planning ahead throughout the year or setting aside money each month can make these larger expenses easier to manage.

8. Get the Kids Involved

Back-to-school shopping is a great opportunity to teach children about budgeting. Give older kids a spending limit and let them compare prices and make decisions within that budget. It's a practical lesson in financial responsibility that can benefit them for years to come.

9. Plan for Unexpected Expenses

School costs don't stop after the first day. Field trips, fundraisers, club dues, picture day, and classroom events often pop up throughout the year. Setting aside a small amount each month in a dedicated savings account can help you prepare for these surprise expenses without disrupting your household budget.

10. Think Beyond August

One of the best budgeting strategies is to prepare year-round. Consider setting up automatic transfers into a dedicated savings account each month so you're ready when the next school year arrives. Even saving $20 to $50 each month can help ease the financial pressure when back-to-school shopping rolls around.

KCCU Can Help You Reach Your Financial Goals

At KCCU, we know every dollar counts. Whether you're building your emergency savings, creating a family budget, or planning ahead for seasonal expenses like back-to-school shopping, having the right financial tools can make a big difference.

Small budgeting habits today can lead to greater financial confidence tomorrow. With thoughtful planning and smart spending, you can help your children start the school year prepared—without putting unnecessary stress on your finances.

Here's to a successful, organized, and budget-friendly school year!

Summer is one of the most popular times of year to travel. School breaks, warm weather, and longer days make it the perfect season for family vacations, beach getaways, road trips, and international adventures. But with peak demand comes higher prices. Flights rise, hotels book quickly, and attractions often charge premium rates during the busiest months.

The good news is that traveling during summer does not have to drain your savings. With careful planning and a few smart strategies, you can enjoy memorable experiences while keeping your budget under control. Whether you are planning a weekend getaway or a two-week vacation, these practical tips can help you save money without sacrificing fun.

Plan Early — But Stay Flexible

One of the easiest ways to save on summer travel is to book early. Airlines and hotels often release lower-priced inventory months in advance, and waiting until the last minute usually means paying more.

However, flexibility can be just as important as early planning. Traveling a few days before or after peak holiday weekends can dramatically lower costs. For example, flying on a Tuesday or Wednesday is often cheaper than departing on a Friday or Sunday.

If your schedule allows, consider traveling during the “shoulder season,” which falls just before or after the busiest summer weeks. Early June and late August can offer lower prices, smaller crowds, and better availability.

Set a Realistic Budget

Before booking anything, create a travel budget that includes transportation, accommodations, food, entertainment, shopping, and emergency expenses. Many travelers underestimate how quickly small purchases add up during a trip.

Having a spending limit helps prioritize what matters most. If your goal is exploring a new city, you may choose a budget hotel and spend more on activities. If relaxation is the priority, investing in a nicer resort while reducing excursions may make more sense.

Tracking expenses during the trip can also prevent overspending. Budgeting apps or even a simple spreadsheet can help you stay on course.

Compare Flight Prices Carefully

Airfare is often one of the biggest travel expenses, especially during summer. Using fare comparison websites and setting price alerts can help you find better deals before prices climb.

A few additional strategies include:

- Checking nearby airports for lower fares

- Booking one-way tickets on different airlines

- Traveling with carry-on luggage only to avoid baggage fees

- Flying early in the morning or late at night when fares are often cheaper

It is also worth reviewing airline reward programs. Even occasional travelers can accumulate points that reduce future travel costs.

Consider Alternative Accommodations

Hotels are not your only option. Vacation rentals, hostels, guesthouses, and home-sharing platforms can provide significant savings, especially for families or larger groups.

Renting a property with a kitchen allows you to prepare meals instead of dining out for every breakfast and dinner. This alone can save hundreds of dollars during a week-long trip.

For road trips or outdoor vacations, camping and RV travel can also be affordable alternatives. Many state and national parks offer scenic campsites at a fraction of hotel prices.

When comparing accommodations, always factor in additional costs like parking fees, cleaning charges, resort fees, and transportation to attractions.

Travel Light

Packing efficiently can save more money than many people realize. Airlines increasingly charge for checked bags, overweight luggage, and seat selection. Traveling with only a carry-on can eliminate many of these fees.

Light packing also makes transportation easier. You may avoid baggage claim delays, expensive taxis, or luggage storage costs.

Choose versatile clothing that can be mixed and matched, and pack reusable essentials such as water bottles, sunscreen, and portable chargers to avoid buying overpriced items at tourist locations.

Save on Food Without Missing Out

Food is a major part of travel, but restaurant costs can quickly spiral out of control. Fortunately, there are plenty of ways to enjoy local cuisine while staying within budget.

Start by balancing restaurant meals with affordable options. Grocery stores, farmers markets, bakeries, and food trucks often provide delicious local flavors at lower prices.

Booking accommodations with free breakfast can also reduce daily expenses. Packing snacks for flights, beach days, or sightseeing adventures helps avoid impulse purchases in tourist areas.

Another smart strategy is eating your largest meal at lunch rather than dinner. Many restaurants offer lunch specials with similar menu items at lower prices.

Use Public Transportation

Rental cars, rideshare apps, parking fees, and fuel costs can significantly increase your travel budget. In many destinations, public transportation is cheaper and more convenient.

Subways, buses, trains, and trams allow travelers to experience cities more like locals while saving money. Many destinations also offer multi-day transit passes that provide unlimited rides for a fixed price.

Walking and biking are excellent alternatives as well. Not only do they reduce costs, but they also allow you to discover neighborhoods and attractions you might otherwise miss.

Look for Free and Low-Cost Activities

A memorable vacation does not have to revolve around expensive attractions. Many destinations offer free experiences that are just as rewarding as paid tours or entertainment.

Popular budget-friendly activities include:

- Public beaches

- Hiking trails

- Museums with free admission days

- Outdoor concerts and festivals

- Historic neighborhoods

- Local markets

- Scenic parks and gardens

Researching local tourism websites before your trip can help uncover hidden gems and free community events happening during your stay.

Protect Yourself from Hidden Costs

Unexpected expenses can quickly ruin a travel budget. Before leaving, review cancellation policies, baggage fees, foreign transaction charges, and mobile roaming rates.

Travel insurance may also be worth considering, especially for expensive trips or international travel. While it adds a small upfront cost, it can protect against major financial losses caused by cancellations, medical emergencies, or lost luggage.

If traveling abroad, using a credit card with no foreign transaction fees can save money on every purchase.

Embrace Slow Travel

Trying to visit too many destinations in one trip often increases transportation costs and creates unnecessary stress. Slow travel — spending more time in fewer places — can lead to both financial savings and a richer experience.

Staying longer in one destination may qualify you for discounted accommodations, lower transportation costs, and a more relaxed itinerary. It also gives you time to discover local restaurants, hidden attractions, and authentic experiences beyond tourist hotspots.

Instead of rushing from city to city, consider choosing one region and exploring it deeply.

Final Thoughts

Summer travel does not need to come with financial regret. The key to saving money is being intentional with your choices. Planning ahead, staying flexible, comparing options carefully, and focusing on meaningful experiences instead of unnecessary extras can make travel both affordable and enjoyable.

The best vacations are rarely defined by luxury alone. Often, the most memorable moments come from discovering a hidden beach, sharing a local meal, exploring a new city on foot, or simply spending quality time with people you care about.

Furthermore, if you’re looking to save while spending on travel, check out KCCU’s Edge Rewards Card. With our Edge Card, you can earn points with the uChoose Rewards program for every dollar you spend and redeem those points for merchandise, travel, and gift cards.

By traveling smarter, you can enjoy everything summer has to offer while keeping your finances healthy long after the trip ends.

May 20th is National Millionaire Day, and to pay tribute to those who wish to join the club, KCCU has created some tips and tricks to help you on the road to success.

How to Become a Millionaire: The Habits, Strategies, and Mindset That Actually Work

Becoming a millionaire is not reserved for celebrities, lottery winners, or tech founders. In reality, most millionaires are ordinary people who consistently make smart financial decisions over a long period of time. They build wealth through discipline, patience, and strategic action rather than overnight success.

The idea of becoming a millionaire can feel overwhelming at first. Many people assume it requires a massive salary, a perfect investment, or extraordinary luck. While high income can help, wealth creation is usually more about behavior than talent. The good news is that the principles of building wealth are straightforward and accessible to almost anyone willing to apply them consistently.

Here’s how to become a millionaire in a practical, realistic way.

Start With the Right Mindset

The journey to becoming a millionaire begins with how you think about money. Wealthy people often see money as a tool rather than something to spend immediately. They focus on long-term growth instead of short-term gratification.

One of the most important shifts is understanding delayed gratification. Instead of constantly upgrading cars, phones, clothes, or lifestyles, future millionaires prioritize investing and saving. They understand that every dollar spent today is a dollar that cannot grow tomorrow.

Another critical mindset shift is taking responsibility for your financial future. Waiting for the perfect opportunity, the government, or an employer to create wealth for you rarely works. Millionaires tend to actively learn about money, investing, taxes, and business opportunities.

Financial success is usually the result of thousands of small, smart decisions compounded over time.

Increase Your Income

There is a limit to how much you can save, but there is far less limit to how much you can earn. Increasing your income is one of the fastest ways to accelerate wealth building.

Start by developing valuable skills. The marketplace rewards people who can solve problems, generate revenue, or provide specialized expertise. Skills in technology, sales, marketing, management, finance, healthcare, and entreprenuership often command high incomes.

You can also increase your earning power by:

- Negotiating your strategy

- Changing industries

- Starting a side hustle

- Freelancing

- Building an online business

- Investing in education or certifications

Many millionaires have multiple income streams. They don’t rely entirely on one paycheck. Additional income sources create flexibility and provide more money to invest.

The goal is not simply to earn more money but to keep more of it and put it to work.

Live Below Your Means

One of the biggest mistakes people make is increasing their spending every time their income rises. This is known as lifestyle inflation.

A person earning $250,000 per year can still live paycheck to paycheck if they overspend. Meanwhile, someone earning far less may quietly build substantial wealth through disciplined saving and investing.

Living below your means creates the gap between income and expenses where wealth grows. That gap becomes your investment capital.

This does not mean you must live miserably or avoid enjoying life. It simply means being intentional with spending. Focus on purchases that genuinely improve your quality of life while avoiding unnecessary debt and status-driven spending.

Many self-made millionaires drive practical cars, live in reasonable homes, and avoid trying to impress others with luxury purchases.

Invest Consistently

Saving money alone rarely creates millionaire-level wealth because inflation slowly reduces purchasing power. Investing is what allows money to grow exponentially over time.

The stock market has historically been one of the most effective wealth-building tools available. Consistently investing in diversified index funds or retirement accounts can produce remarkable long-term growth.

Compound interest is the key. When your investments generate returns, and those returns begin generating their own returns, wealth starts accelerating.

For example, someone who invests $500 per month consistently over several decades can accumulate over a million dollars depending on market performance.

The earlier you start, the more powerful compounding becomes.

Real estate is another common path to wealth. Rental properties can create cash flow, appreciation, and tax advantages. Some millionaires also build wealth through businesses, private investments, or entrepreneurship.

The important thing is consistency. Successful investors continue investing during good markets and bad markets alike.

Avoid Bad Debt

Not all debt is equal. Some forms of debt can help build wealth, while others destroy financial progress.

High-interest consumer debt—especially credit card debt—is one of the biggest obstacles to becoming wealthy. Paying 20% interest on purchases works against everything investing tries to accomplish.

Millionaires generally avoid carrying large balances on depreciating assets. Instead, they use debt strategically when it helps generate future value, such as buying a business, investing in education, or purchasing income-producing real estate.

If you currently have high-interest debt, paying it down aggressively may provide one of the best returns on investment available.

Build Long-Term Discipline

Most people underestimate how long wealth building takes. Social media often promotes unrealistic stories of instant success, but sustainable wealth usually develops slowly.

The path to becoming a millionaire often looks boring:

- Saving consistently

- Investing regularly

- Avoiding unnecessary debt

- Increasing income gradually

- Staying patient during market downturns

Discipline matters more than intensity. A person making steady financial progress for 20 years will often outperform someone chasing risky shortcuts.

There will be setbacks along the way. Markets crash. Businesses fail. Unexpected expenses happen. The people who ultimately build wealth are the ones who continue moving forward despite temporary obstacles.

Surround Yourself With Financially Smart People

Your environment strongly influences your financial behavior. If everyone around you spends recklessly, avoids investing, or dismisses long-term planning, it becomes harder to stay disciplined.

Seek out people who understand money, business, investing, and growth. Read books from respected financial thinkers. Listen to educational podcasts. Learn from people who have already achieved the results you want.

Financial literacy compounds just like money does.

Final Thoughts

Becoming a millionaire is less about luck and more about consistent habits repeated over time. The formula is surprisingly simple: earn more, spend less than you earn, invest the difference, and stay patient.

You do not need a perfect background, a six-figure salary, or a groundbreaking business idea to build wealth. What you need is a long-term perspective and the willingness to make smart financial decisions consistently.

Wealth is rarely built overnight, but with discipline and persistence, becoming a millionaire is far more achievable than most people realize.

Getting pre-approved for a mortgage isn't just a step, it's your secret weapon to becoming the buyer sellers actually want to work with.

In 2026's real estate market, pre-approval is more important than ever. Here's why: sellers are receiving multiple offers, and they want to work with buyers they can trust. A pre-approval letter tells them you're serious. You've already gone through the financial vetting process. A lender has reviewed your income, credit score, debt, and assets—and given you the green light. That's powerful.

Without pre-approval, you're essentially asking sellers to take a gamble on you. Will your financing actually come through? Does your income really match what you're claiming? Are you actually qualified to borrow that much? Pre-approval answers all those questions upfront. It's not a maybe—it's a verified yes from a professional lender.

Know Your Real Budget (No More Guessing Games)

Let's be honest—buying a home is emotional. You see the perfect place online, and suddenly you're imagining yourself living there. But without knowing your actual budget, you might fall head over heels for a house that's completely out of reach financially.

Pre-approval fixes this. When you get pre-approved, you'll learn exactly how much lenders are willing to let you borrow. Let's walk through a real scenario:

You think you can afford a $350,000 home. You've been saving, you have a decent job, and your credit score is solid. But when you sit down with KCCU for pre-approval, the lender reviews everything. Your income, your student loans, your car payment, your credit history, your down payment savings—all of it. After the full analysis, they tell you: "We can approve you for $320,000." That might be disappointing at first, but here's why it matters: that number is based on real financial facts, not wishful thinking. Mortgage lenders want to make sure that you can afford your payment and not be too strapped for cash.

Now you know. You can shop confidently for homes in the $300,000 range (giving yourself some breathing room). You won't fall in love with a $400,000 home only to have your loan application rejected. You won't get to closing day and realize you can't actually afford the monthly payments. You won't lie awake at night worried about whether you made a huge financial mistake.

This clarity is everything. It lets you focus your energy on homes you can actually buy. Plus, knowing your budget helps you negotiate smarter. If a home is listed at $310,000 and you know you're pre-approved for $320,000, you understand your negotiating power.

The Sellers' Perspective: Why Your Pre-Approval Letter Is Your Golden Ticket

Here's something most first-time buyers don't realize: sellers care about pre-approval almost as much as you should.

When a seller receives multiple offers in 2026, they're making a tough choice. Sure, one offer might be $5,000 higher than another. But if that higher offer comes from a buyer without pre-approval, and the lower offer comes from a pre-approved buyer, many sellers will take the lower offer. Why? Because the lower offer is certain. The pre-approved buyer is less likely to have financing fall through.

Think about it from the seller's perspective: they're about to hand over the keys to their home. They need to know the deal will actually close. They've already accepted your offer, so they've stopped showing the home to other buyers. Their real estate agent is preparing the paperwork. Everyone's counting on you to secure financing. If your loan falls through at the last minute, they're back to square one—and they've lost weeks.

Pre-approval dramatically reduces that risk. It tells sellers: this buyer is legit. This buyer has already proven their finances to a professional lender. The financing isn't a question mark, it's locked in. You're the safe choice, the buyer they want to work with. That might be the difference between your offer being accepted or rejected.

Getting Pre-Approved vs. Pre-Qualified: Why the Difference Matters

You might have heard both terms thrown around, and they sound similar. But they're very different, and understanding the difference could save you from embarrassment later.

Pre-qualification is a rough estimate. You give a lender basic information about your income and credit, and they tell you a ballpark figure of what you might be able to borrow. It takes 15 minutes, and it's not binding. It's helpful for getting a general sense of your budget, but it's not a promise. The lender hasn't verified anything. They're taking your word for it.

Pre-approval is the real deal. You've provided documentation—pay stubs, tax returns, bank statements, proof of employment. The lender has pulled your credit report and verified everything you've told them. They've checked your debts, your assets, your employment history. After all that verification, they've decided: yes, we will lend you this amount of money. It's a commitment, not a guess.

So if you're serious about buying in 2026, skip pre-qualification and go straight to pre-approval. It takes a bit longer (usually a few days), but it's absolutely worth it.

What Happens Next: Your Path from Pre-Approval to Keys in Hand

Getting pre-approved is a major milestone, but it's not the finish line. Let's walk through what comes next so you feel confident about the journey.

Step 1: You've got your pre-approval letter. This is valid for about 90 days. You can now start house hunting with confidence.

Step 2: You find a home you love and make an offer. Your real estate agent includes your pre-approval letter with your offer. Sellers see it. You're competitive.

Step 3: Your offer is accepted. Congratulations! Now the real work begins. You and the seller agree on a closing date (usually 30-45 days away).

Step 4: You move to full mortgage approval. This is when you work more closely with your lender at KCCU. You'll do a home inspection, get a professional appraisal done, and finalize your loan terms. The lender wants to make sure the home is worth what you're borrowing.

Step 5: Final walkthrough and closing. A few days before closing, you walk through the home one more time to make sure everything agreed upon is still in place. Then you sign paperwork, provide your down payment, and get your keys.

The whole process from pre-approval to keys in hand usually takes 40-60 days. Your KCCU team will guide you through every step, answer your questions, and keep things moving forward. You won't feel lost or confused because you'll have a professional in your corner.

Ready to Get Pre-Approved? Here's How KCCU Makes It Easy

If you're ready to stop wondering and start knowing your real buying power, getting pre-approved with KCCU is simpler than you think.

Here's what you need to do:

- Gather your documents: Have recent pay stubs, your last two years of tax returns, bank statements showing your savings, and your ID ready. Don't worry if you don't have everything perfect—KCCU can help you figure out what you need.

- Contact KCCU: Reach out to our mortgage team. You can call, email, or apply online. Whatever feels easiest for you.

- Have a conversation: A mortgage specialist will talk through your situation, answer your questions, and explain the process. This isn't intimidating—it's a friendly chat with someone who's helped hundreds of buyers.

- Submit your application: You'll provide your financial information, and KCCU will verify everything with employers, banks, and credit bureaus.

- Get your pre-approval letter: Within a few business days, you'll have your letter in hand. You're officially ready to make an offer.

The best part? KCCU is a credit union, and we care about your financial health. Our mortgage specialists will be honest with you about what makes sense for your situation. They'll help you understand your options and find a loan that works for your life—not just today, but five, ten, twenty years from now.

Getting pre-approved isn't just about jumping through hoops. It's about taking control of your homebuying journey. It's about walking into negotiations from a position of strength. It's about knowing, without a doubt, that when you find the right home, you can actually buy it.

Stop wondering if you're ready to buy. Let KCCU show you that you are. Contact our mortgage team today and take the first step toward owning your home.

If you've had the same auto loan for more than a year, you could be leaving a significant amount of money on the table every single month.

Back in 2023 through early 2025, interest rates were climbing. If you locked in your auto loan during that period, you're probably paying a higher rate than what's available today in 2026.

Let's talk real numbers. Say you financed a $25,000 car at 7.5%APR* with a 60-month loan twelve months ago. Your monthly payment is around $501 and you’d pay roughly $5070 in interest over the life of the loan. Now imagine refinancing that same loan. Since you have now paid down your loan for 12 months, you’d roughly owe $20,750 and you can refinance it for 48 months at today's rate of 4.99%APR*. Your new monthly payment drops to roughly $477 which is $24 less per month, but with that savings you are only paying $2,150 over the life of the loan for the remaining 48 months, that is a huge savings over $5,070!!

The best part? You don't have to guess whether refinancing makes sense for your specific situation. We'll walk you through the math in just a few minutes, and you'll have a clear answer.

What Refinancing Actually Means (It's Simpler Than You Think)

Refinancing sounds like it should be complicated, but it's actually pretty straightforward.

Think of it this way: you currently have an auto loan from another lender. That lender gave you money to buy your car, and you're paying them back with interest. Refinancing means you're replacing that old loan with a new loan from a different lender—in this case, KCCU—at better terms.

Here's what happens behind the scenes:

- KCCU pays off your old loan completely

- You now owe KCCU instead of your old lender

- Your car title and registration stay the same

- You make monthly payments to KCCU at your new, lower rate

That's it. There's no magic trick, no hidden catch. You're just moving your debt to a lender offering better terms.

The only real change in your life is that you'll be sending your payment to KCCU instead of your old lender, and you'll likely be paying less interest overall. Which, honestly, sounds pretty good.

The KCCU Advantage: Rates and Benefits You Won't Find Everywhere

So why refinance with KCCU specifically? Because member-owned credit unions typically offer benefits that traditional banks can't match, and KCCU is no exception.

Competitive 2026 rates. Currently KCCU members can qualify for auto refinance rates starting as low as 4.74%APR* for qualified borrowers. If your current rate is anything above 6%, you're definitely in the running for a better deal. Even moving from 7% to 5.5% saves thousands.

Streamlined online application. You can start your refinance application at any time, from anywhere - even your couch, at midnight, on a Saturday! KCCU's online loan application is designed to be quick and easy.

Member-exclusive perks. Depending on your membership status and account history, KCCU may offer rate discounts for being loyal members.

Flexible loan terms. You're not locked in to a specific timeline. Whether you want to keep your current 60-month term or accelerate it to 48 months (and pay it off faster), KCCU works with you. Shorter terms mean less interest paid overall, if that's your goal.

Real customer service. Because KCCU is member-owned, there's actual incentive to help you succeed. You're not a number in a database; you're a member. If you have questions during the process, you'll talk to real people, who lives locally who can explain your options clearly.

Calculate Your Real Savings (Use Our Simple Method)

Okay, let's make this personal. Here's how to calculate your exact potential savings with just four pieces of information from your current auto loan.

What you need:

- Your current interest rate (check your loan statement)

- Your current monthly payment

- Your remaining loan balance (not the car's value—just what you still owe)

- How many months are left on your loan

Use KCCU’s handy dandy auto loan calculator to see your exact potential savings, done swiftly and simply using the four pieces of information above.

The Refinancing Process at KCCU: Start to Finish in 5 Steps

Here's the thing about refinancing: the actual process is way less complicated than most people expect. KCCU has designed it to be as simple as possible. Here's exactly what happens.

Step 1: Gather Your Documents (10 minutes)

You'll need a few things, but nothing crazy:

- Your social security number and driver license if you are not a member

- Your current auto loan statement (to verify remaining balance and lender info)

- Your vehicle's VIN (on your registration or dashboard)

- A recent pay stub or tax return (to verify income)

- Proof of insurance

Take a photo of these if you're applying online, or bring originals if you visit in person.

Step 2: Apply Online or In Person

Head to KCCU's website and start the refinance application. Or feel free to visit a KCCU branch near you—a representative can walk you through the process in person if you prefer that human touch.

Step 3: Get Approved and Review Terms

KCCU will review your application, check your credit score, and verify the vehicle information. In most cases, you'll hear back within the same business day. They'll give you a formal offer with your exact interest rate, monthly payment, and loan terms. Read through it carefully—there shouldn't be any surprises, but it's your money, so make sure everything matches what you expected.

Step 4: Sign Digital or Paper Documents

Once you approve the offer, you'll sign the loan documents. KCCU offers digital signing, which is fast and secure. No need to print anything or make a trip unless you prefer to. You can sign from your phone in literally two minutes.

Step 5: KCCU Pays Off Your Old Loan and You're Done

KCCU handles the payoff of your old loan. They contact your previous lender, send the money, and handle all the paperwork. You don't have to do anything. Your first payment to KCCU will be due according to the schedule you agreed to.

Common Concerns (And Why You Shouldn't Worry)

Before you move forward, let's address the stuff that typically makes people hesitate. These are legitimate questions, and they deserve honest answers.

Will refinancing hurt my credit score?

A little bit, yes—but not in the way you think. When KCCU pulls your credit to review your application, there's a small dip, but it is temporary and normal. But here's what matters: refinancing actually helps your credit long-term because you're reducing your overall debt and showing you can manage new credit responsibly. The small, short-term dip is worth it. Within a few months, your score typically bounces back higher than before because of improved credit metrics. Don't let a tiny temporary dip stop you from saving thousands.

What if there's an early payoff penalty on my current loan?

First, check your loan documents. Most auto loans don't have prepayment penalties, but some older loans might. If yours does, find out the exact amount. Then, do the math: subtract that penalty from your total refinance savings. If you're still coming out ahead (which you probably will), the penalty is just a one-time cost that pays for itself within a few months of lower payments. If the penalty is huge and your savings are small, hold off—but this is rare.

What if I want to pay off my loan early? Can I do that with KCCU?

Absolutely. KCCU doesn't penalize early payoff. Pay $500 one month if you can, or throw bonuses toward the principal—no restrictions. You can actually accelerate your payoff timeline and save even more on interest. This is one of the benefits of working with a member-owned credit union.

Is refinancing really worth it if I only have a year left on my loan?

Maybe, maybe not. Run the numbers using the calculation method earlier. If you're saving less than $500 total, the hassle might not be worth it. But if you're saving $800 or more, it's worth the small amount of time and effort it takes. There's no magic cutoff—it depends on your specific numbers. That's why doing the math matters.

What if my credit score isn't great?

KCCU works with borrowers across the credit spectrum. If your score has improved since you got your original loan, you probably qualify for better rates. Even if your score isn't perfect, refinancing might still make sense. The only way to know is to apply—there's no obligation, and checking doesn't lock you in.

Ready to Refinance? Your Next Move

You've done the reading. You've run the numbers (or you know how to). You understand the process and there are no mysteries left. The only question now is: how much money do you want to save?

If your calculation showed you're saving $500 or more, refinancing is a no-brainer. If you're saving less than that, think about whether the effort is worth the payoff—but don't dismiss it out of hand.

Here's how to get started with KCCU:

- Apply online: Visit KCCU's website and click on "Auto Loans." You can start your application right now, no appointment needed.

- Call KCCU: Speak with a real person who can answer questions specific to your situation at 800.854.5421

- Visit in person: Stop by a KCCU branch near you. A Member Service Representative can walk you through everything and answer questions on the spot.

The worst that happens? You get approved, run the numbers again, and decide it's not the right time. You're out nothing. The best that happens? You lock in a lower rate, start paying less every month, and save thousands of dollars with minimal effort.

Reach out to KCCU today and find out exactly how much you could save. Your future self (and your monthly budget) will thank you.

*APR=Annual Percentage Rate. Rate is effective as of April 14, 2026. Minimum credit score 730 for best rate. Advertised rate includes a 0.25% APR discount for members who redeem 20,000 VIP Lifetime Reward Points. If sufficient VIP points are not available, the 0.25% rate discount will not apply. Other rates and terms available. Loan is subject to credit approval. Rate may vary based on credit history, term, and collateral. Loan programs, rates, terms, and conditions are subject to change at any time without notice. Other restrictions may apply.

If you already have a KCCU individual retirement account (IRA), you’re on the right track. But simply having an account isn’t enough—the real advantage comes from how you use it. Small, consistent decisions in 2026 can make a significant difference in how much you have when retirement arrives.

What Makes a KCCU IRA Valuable

KCCU IRA accounts are designed to give members flexible, tax-advantaged ways to save for retirement. Whether you choose a traditional or Roth IRA, you gain access to a range of investment options and personalized support to help guide your decisions. KCCU also makes it easy to manage your account, set up automatic contributions, and consolidate outside retirement funds, which can simplify your overall financial picture. This combination of flexibility, accessibility, and local support makes KCCU IRAs a strong foundation for long-term retirement planning.

Know Your Contribution Limits—and Aim to Max Them Out

For 2026, IRA contribution limits are:

- $7,000 if you’re under age 50

- $8,500 if you’re 50 or older

These limits define how much you can grow your money with tax advantages each year. The closer you get to the maximum, the more you benefit from compounding. If contributing a lump sum isn’t realistic, setting up automatic monthly transfers can help you steadily reach the limit.

Choose the Right Tax Strategy

IRAs come with two primary tax options, and choosing the right one can impact your finances both now and in retirement.

- Traditional IRA: Contributions may reduce your taxable income today, but withdrawals in retirement are taxed.

- Roth IRA: Contributions are made after taxes, but growth and qualified withdrawals are tax-free.

If you expect to be in a higher tax bracket later, a Roth IRA may offer more long-term value. If you prefer immediate tax savings, a traditional IRA might be the better fit. Many savers use both to balance current and future tax benefits.

Make Sure Your Contributions Are Invested

Contributing alone isn’t enough—your funds need to be invested to grow.

A simple guideline:

- 20s–30s: focus on stocks for growth

- 40s–50s: use a balanced mix

- Near retirement: shift toward more stable investments like bonds

If you prefer a hands-off approach, target-date funds automatically adjust your investment mix over time.

Consolidate Old Retirement Accounts

If you have old 401(k)s or IRAs from previous jobs, consolidating them into your KCCU IRA can simplify your finances and reduce fees. A direct rollover helps you avoid taxes and penalties while bringing everything into one place for easier management.

Use Dollar-Cost Averaging to Stay Consistent

Rather than trying to time the market, invest steadily over time. Monthly contributions allow you to buy at different price points, helping reduce risk and smooth out volatility. Automating your deposits makes consistency easy.

Take Advantage of Spousal IRAs

If you’re married, both partners can contribute to IRAs—even if only one earns income. This can significantly increase your household’s retirement savings and provide more flexibility in managing taxes later on.

Review and Adjust Each Year

Your IRA strategy should evolve with your life. Once a year, take time to:

- Review contributions and progress

- Check your investment allocation

- Rebalance if needed

- Adjust for any life or income changes

Regular check-ins help ensure your plan stays aligned with your goals.

Build Consistency for Long-Term Results

Maximizing your IRA doesn’t require complex strategies—just consistent action. Contribute regularly, invest wisely, and revisit your plan each year.

By focusing on key habits—maxing out contributions, choosing the right tax approach, investing appropriately, consolidating accounts, automating savings, and reviewing annually—you set yourself up for long-term success.

Retirement may feel far away, but the steps you take today will shape your future. Start now, stay consistent, and let your KCCU IRA work for you over time.

If you live, work, worship, or attend school in Michigan, KCCU is an option for you. Starting a membership is easy; all you need is a $5 deposit. You don't need a Kellogg's cereal commection, no Battle Creek address, and we definitely don't require you to jump through any hoops.

If you've never been a member of a credit union, we bet you have a lot of questions about the process of joining, and what makes it different from opening a bank account. We'll walk you through it all - from who qualifies, to what joining looks like, and why thousands of Michigan residents have made KCCU their financial home for decades.

Do I Have to Work at Kellogg's to Join KCCU?

Who is Eligible to Join KCCU?

You are eligible to join KCCU if you:

- Live in Michigan

- Work in Michigan

- Worship in Michigan

- Attend school in Michigan

- Own/operate a business in Michigan

Relatives of KCCU members are also eligible for membership with us! Regardless of where you live or work, if your family member is a member, you are eligible as well.

What's the Difference Between Joining a Credit Union and Opening a Bank Account?

You're an Owner, Not Just a Customer

The idea of “joining” a financial institution might feel unfamiliar if you’ve only ever used big banks to manage your money. The key distinction of joining a credit union is that you become a part-owner of the establishment instead of simply being a customer.

“When you become a member at KCCU, you are simply opening an account like you would with a bank,” Rori Ross, Vice President of Marketing at KCCU, explains. “The main difference is that when you open an account, you become a member and part-owner of KCCU. You must deposit $5 in your savings account upon opening the account and keep that $5 in the account. That’s your membership/ownership share in the credit union.”

What That Means For Your Money

Unlike banks, credit unions are not-for-profit. Profits are returned to members by way of reduced fees, higher savings rates, and lower loan rates.

At a bank, the profits go to outside shareholders. At KCCU, they come back to you.

“Credit unions are member-owned, whereas banks are owned by shareholders,” Ross says. “Our executive team reports to a voluntary board of directors who have our members’ best interest in mind, compared to banks who have shareholders and are more profit-driven.”

How Do You Actually Join a Credit Union?

What to Bring

Joining KCCU is very simple. Stop by any branch and speak with a Member Service Representative, and bring your Social Security card and one of the following:

- Driver's license

- State-issued ID card

- Travel visa

- Passport

From there, KCCU membership requires a minimum savings account deposit of only $5.

What to Expect

“Opening an account at KCCU is simple and quick,” Ross notes. “Typically, we can open an account in 30 minutes, but that may vary depending on what products and services are being opened. You will leave with a KCCU membership card and other account documentation. Once you’re a member, you have access to all of our products and services.”

And that’s it. Just bring your ID, Social Security card, $5, and you’re all done. From that point forward, you’re a member-owner of a financial institution that’s been serving Michigan since 1941.

Once a Member, Always a Member. What Does That Mean?

Your KCCU Membership Follows You for Life

One of the most meaningful benefits of credit union membership is something called the “Once a Member, Always a Member” policy. This means you’ll have access to KCCU’s products and services for a lifetime, even if you retire, change jobs, or relocate.

Your membership gets locked in the moment that you join. If you want to move to another state 10 years down the road, you don’t have to requalify or look for another financial institution. You are a KCCU member for life.

Why Members Stay

This lifetime membership quality is why we have members that stay with us for 30, 40, even 50 years.

“Many long-time members enjoy the low turnover rate with our employees,” Ross explains. “They appreciate being treated with kindness, patience, and care, and they recognize our professionalism. Furthermore, several long-time members see our staff as more than consultants and tellers, they see them as family.”

What Can You Do as a KCCU Member?

Many people think that, since credit unions are smaller operations than banks, they don’t (or can’t) offer as much as a big bank does. That is not the case at KCCU.

“There may be some misconception because we are a local credit union. People may think that we don’t offer all the services of a large bank, but we do. Sometimes, we offer even more. We are truly a one-stop shop for all financial needs. And we do it with personalized, local service.”

A Full Look at KCCU's Products and Services

Here’s a quick rundown of what KCCU offers:

- Checking and savings accounts (including a high-yield eChecking account)

- Auto, boat, and RV loans

- Mortgages and home equity loans

- Personal (signature) loans and credit cards

- Business checking and commercial lending

- Certificates of deposit (CDs) and IRAs

- Investment services through LPL Financial

- Insurance products

- A full digital banking suite (that includes online banking, a mobile app, mobile deposit, bill pay, text banking, and more)

Your Money is Protected

Your money is just as safe here as it would be at any bank. KCCU is federally insured by the National Credit Union Administration (NCUA), which is the credit union equivalent of the FDIC, and it insures deposits up to $250,000.

KCCU has also been recognized by Newsweek as one of America’s Best Credit Unions for three years running, which speaks to the quality and consistency that our members experience.

Why Would People Choose a Credit Union Over a Big Bank?

Our Service is Personal

“Many people have transitioned from a big bank to our credit union because of their positive experiences with our personal service, lower fees, and competitive rates. We often hear from individuals that they felt like, at a bank, they were just a number. But, at KCCU, we treat them like family and have their best interest in mind,” says Ross.

“Being a member at KCCU goes beyond just a bank account,” Ross continues. “Being a member at KCCU means walking into your favorite branch to team members who offer a warm smile, and who are excited to greet you and ask how you’ve been. We’re your biggest cheerleaders, financial consultants, neighbors, friends, and family.”

The Financial Benefits

Because KCCU is a not-for-profit cooperative, it is able to offer lower loan rates and higher savings rates than many big banks. Those benefits go directly back to the people who bank at a credit union.

Are You Ready to Make the Switch?

“At KCCU, we can be the one stop for all of your financial needs,” Ross says. That’s what she most wants potential new members to understand. “We will always have your best interests in mind. KCCU is a local organization, and the team that serves you lives, works, and supports your local community.”

Getting started is as easy as stopping by any KCCU branch and bringing your ID, Social Security card and $5. You can also visit kccu4u.org to learn more about membership, explore rates, and see everything else that KCCU has to offer.

Tax season can feel overwhelming, but with the right preparation, it doesn’t have to be stressful. Staying organized and starting early can help you avoid mistakes, reduce anxiety, and potentially maximize your refund. Use this tax season checklist to make sure you are fully prepared.

1. Gather Personal Information

- Social Security numbers or Tax Identification Numbers for you, your spouse, and dependents

- Dates of birth for everyone listed on your return

- Your previous year’s tax return for reference

2. Collect Income Documents

Gather all documents that report income earned during the year. These may include:

- W-2 forms from employees

- 1099 forms for freelance, contract, or other non-employee income

- 1099-INT or 1099-DIV for interest and dividends

- 1099-R for retirement distributions

- Records of rental income or other miscellaneous income

3. Organize Expense Records

If you plan to itemize deductions or claim credits, collect documentation for eligible expenses, such as:

- Mortgage interest statements

- Property tax statements

- Charitable donation receipts

- Medical expense records

- Education expenses and tuition statements

4. Review Tax Credits and Deductions

Consider whether you qualify for common tax credits and deductions, including:

- Child Tax Credit

- Earned Income Tax Credit

- Education credits

- Retirement savings contributions credit

- Energy-efficient home improvement credits

5. Prepare Business or Self-Employment Records

If you are self-employed or own a small business, gather:

- Income and expense records

- Mileage logs

- Receipts for business-related purchases

- Home office expense documentation

- Quarterly estimated tax payment records

6. Verify Bank Information

If you are expecting a refund or plan to pay electronically, confirm your bank account and routing numbers to avoid processing delays.

7. Check Important Deadlines

Mark important tax deadlines on your calendar. Filing late can result in penalties and interest. If you need more time, consider filing for an extension before the due date.

8. Choose How You Will File

Decide whether you will:

- File your taxes using tax software

- Work with a certified tax professional

- Use free filing options if you qualify

9. Review Before Submitting

Before submitting your return, carefully review:

- Names and Social Security numbers

- Income amounts

- Deductions and credits claimed

- Bank account details

10. Keep Copies of Everything

After filing, keep copies of your tax return and all supporting documents in a secure location. These records may be needed for future reference or in case of an audit.

Final Thoughts

Tax season does not have to be complicated. By following this checklist and staying organized throughout the year, you can approach tax filing with confidence and peace of mind.

February, the month for boxed chocolates, red roses, and romance. Yes, love indeed scatters itself through the air, especially during this time of year, but one kind of “romance” is always on the prowl: online romance scams. As human beings, we crave connection, safety, and trust. At first, an online romance scam may seem like it checks all three of these boxes, but in reality, the only connection they’re seeking is money from your bank account being transferred to theirs. According to Eyewitness News, the FBI reported more than $635 million was lost to online romance scams in 2025, indicating a substantial amount of victims were affected. At KCCU, we want our members’ hearts and wallets protected from those who attempt to seek advantage. We’re here to help point out all the signs of an online romance scam, from start to finish.

In this blog, we’ll break down what online romance scams are, how they operate, warning signs to watch for, and practical steps to protect yourself and loved ones. If you use dating apps, social networks, or messenger platforms, this guide is essential reading.

What Are Online Romance Scams?

An online romance scam occurs when a fraudster creates a fake identity to pursue a romantic relationship with someone online with the ultimate goal of obtaining money, personal information, or both. Unlike other scams that might be one-off transactions, these cons build emotional bonds first and then exploit them.

Scammers typically initiate contact through dating sites, social networking platforms, or messaging apps. Over time, they cultivate what appears to be a genuine emotional connection, then gradually introduce financial requests under various pretenses.

Why Romance Scams Work

Romance scams succeed because they manipulate basic human needs: love, affection, loneliness, and trust. Many victims are seeking companionship and may be more open to expressions of love and emotional support. Scammers exploit these vulnerabilities by mirroring desires - flattering, supportive, and engaging consistently until the victim begins to trust them.

Once trust is established, the requests for money or help don’t sound like demands, they sound like needs of someone you care about.

How Scammers Build the Illusion of Love

A common thread in these schemes is emotional investment. Here’s a typical sequence:

- Initial Contact

The scammer sends a message or friend request, sometimes triggered by a profile that seems ideal for each other. - Rapid Emotional Intimacy

Without ever meeting in person, they express affection quickly, often using phrases like “I think I’ve found my soulmate in you.” - Frequent Communication

They message daily, sometimes hourly, to establish a sense of closeness and routine. - Isolation Tactics

They encourage the victim to keep the relationship private to avoid questioning from friends and family. - Fabricated Crises or Needs

Once trust is strong, they request financial help: to pay a medical bill, travel expenses, legal fees, or unexpected emergencies. - Refusal to Meet in Person

When asked to video chat or meet, they invent reasons, travel schedules, work obligations, cultural norms, designed to avoid verification of identity.

By orchestrating emotional dependence and gradual escalation, scammers make their requests seem legitimate.

Common Scenarios and Excuses

Scammers will deploy a variety of stories. Some of the most common include:

- Emergency medical situation — “I have no money to pay my doctor.”

- Travel delay or problems at the border — “I need cash to get my passport back.”

- Job or business investment opportunity — “This will secure our future.”

- Family crisis — “My child is sick.”

In each case, the scenario is designed to evoke empathy and urgency.

Who Gets Targeted? It’s Broader Than You Think

While scammers can target anyone, certain factors increase vulnerability:

- People seeking companionship after loss or divorce

- Individuals isolated by geography, disability, or circumstance

- Older adults who may be less familiar with digital communication

- Users of niche dating platforms (military, religious, hobby-oriented) where assumed shared interests build trust faster

But even experienced internet users can be pulled in; these fraudsters are adept at psychology, persistence, and manipulation.

Financial and Emotional Impact

The financial losses from romance scams are staggering. In many countries, authorities report billions of dollars lost annually to online romance fraud. Scammers often extract money slowly to avoid suspicion, perhaps sending multiple smaller requests that add up over time.

The emotional toll can be even deeper:

- Shame and embarrassment at being deceived

- Trust issues with future relationships

- Isolation and withdrawal from social support networks

The deception doesn’t just take money; it undermines confidence and emotional well-being.

Red Flags: Spotting a Romance Scam

Recognizing a scam early can save both your heart and your finances. Here are common warning signs:

1. The Connection Happens Too Fast

They profess deep feelings early in the conversation after only a few days or weeks.

2. They Avoid Face-to-Face Verification

Repeated excuses for avoiding video calls or in-person meetings.

3. They Ask to Move Away From the Platform Quickly

Suggesting you switch to email, private messaging apps, or SMS before sufficient trust is built.

4. Their Photos Are Too Perfect

Pictures resemble professional models or appear syndicated across multiple profiles (reverse image search can reveal reuse).

5. They Request Money

Especially for emotional or personal crises.

6. Their Stories Don’t Add Up

Conflicting details or evasiveness about specific personal information.

7. They Claim to Be Abroad or Traveling Constantly

Frequent “international” explanations that make logistics implausible.

Protect Yourself: Practical Safety Tips

Here’s how you can protect yourself and others from romance scam situations:

Take It Slow: Meaningful connections take time. Don’t rush into deep emotional disclosures.

Verify Identity: Use video calls early in communication before trust becomes too strong to question.

Do a Reverse Image Search: This can reveal whether a photo is scraped from stock sites or someone else’s social media.

Never Send Money: No matter how compelling the story sounds. Once money is sent, it’s often impossible to recover.

Keep Communication on the Platform: Dating sites and apps often provide some level of monitoring and accountability.

Talk to Friends or Family: Independent perspectives often spot inconsistencies you might overlook.

Learn the Common Scammer Playbooks: Understanding typical tactics makes you less susceptible to manipulation.

What If You’ve Been Scammed? Steps to Take

- Cease all communication with the scammer.

- Report the profile to the platform.

- Report to relevant authorities

These reports help track patterns and protect others.- Federal Trade Commission (FTC): The main place to report identity theft, scams, and unethical business practices; they use reports for law enforcement.

- FBI’s Internet Crime Complaint Center: For all internet-enabled crimes, helping with investigations and fund recovery.

- Inform your bank or financial institutions immediately if you’ve transferred money.

- Talk to someone you trust — emotional support is crucial.

- Seek professional advice if necessary, especially if financial loss is significant.

Why Reporting Matters

Many victims don’t report scams due to shame or fear of judgment. But reporting is critical:

- It helps law enforcement track organized fraud rings.

- It can protect others from falling into the same trap.

- It contributes to public awareness and better safety practices on platforms.

Remember: the fault lies with the scammer, not the victim.

Final Thoughts: Love Isn’t a Scam, But Be Smart

Online romance scams are real, sophisticated, and emotionally wrenching. They prey on compassion and trust. But awareness is power. By understanding common tactics, recognizing red flags, and prioritizing safety, you can enjoy digital connections with confidence.

Love shouldn’t cost you your savings or your self-worth.

Stay informed. Stay cautious. And when in doubt, reach out for support. Your heart and wallet will be better off for it.

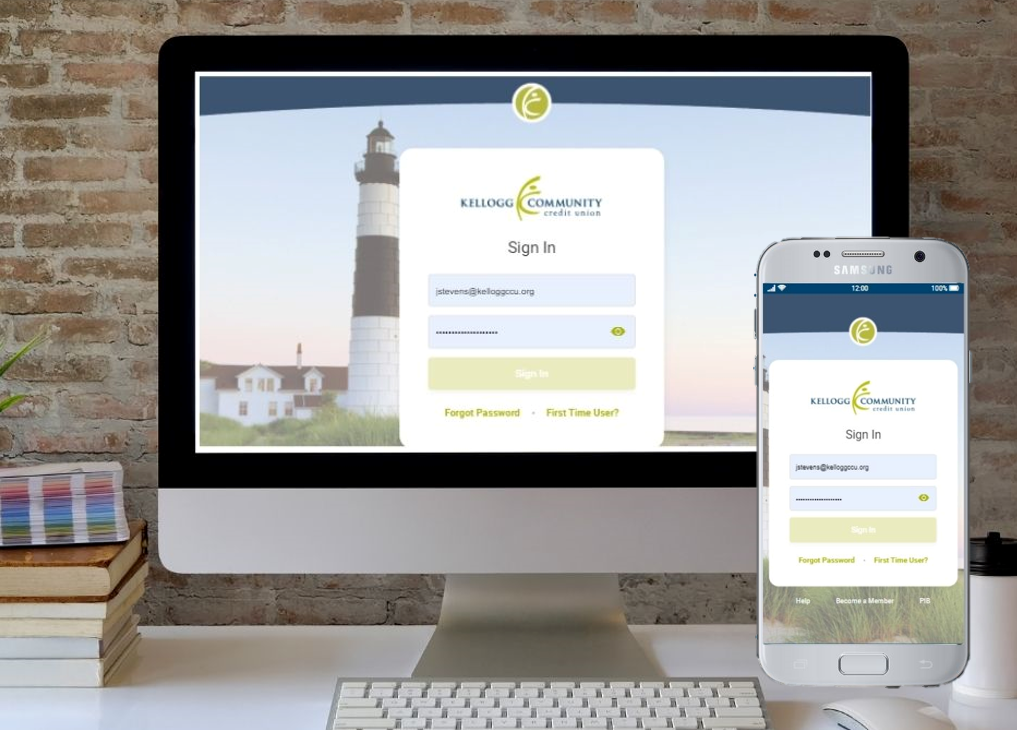

In today’s digital world, protecting your personal and financial information is more important than ever. From online banking to mobile apps and social media, our data is constantly in motion. At KCCU, your security is a top priority—and there are simple steps you can take to strengthen your own data privacy every day.

1. Use Strong, Unique Passwords

2. Enable Multi-Factor Authentication (MFA)

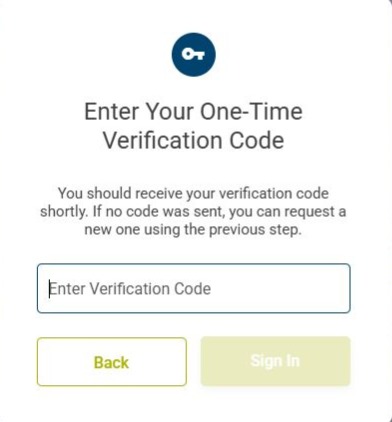

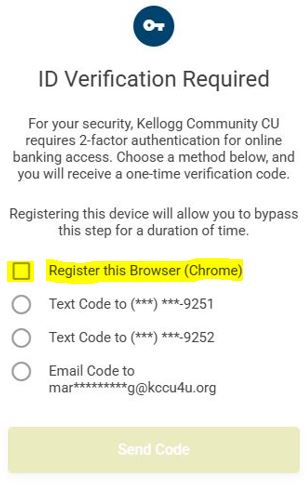

Whenever possible, turn on multi-factor authentication. This adds an extra layer of security by requiring a second verification step—such as a one-time code—before accessing your account.

3. Be Alert to Phishing Attempts

Fraudsters often pose as trusted organizations to trick you into sharing sensitive information. Be cautious with emails, texts, or calls that ask for personal or financial details. KCCU will never ask for your login credentials through unsolicited messages.

4. Keep Your Devices Updated

Regularly update your phone, computer, and apps. Updates often include important security patches that protect against the latest threats.

5. Review Privacy Settings

Check the privacy and security settings on your banking apps, social media, and other online services. Limit the amount of personal information you share publicly and only grant app permissions that are truly necessary.

6. Use Secure Networks

Avoid accessing financial accounts on public Wi-Fi. If you must use a public network, consider a trusted virtual private network (VPN) to encrypt your connection.

7. Monitor Your Accounts Regularly

Review your bank and credit card statements frequently. If you notice anything unusual, report it to KCCU immediately so action can be taken quickly.

8. Safely Dispose of Sensitive Information

Shred documents containing personal or financial details before discarding them. This simple habit can prevent identity theft.

Staying informed and proactive is one of the best ways to protect your data. By following these tips and partnering with KCCU’s commitment to security, you can bank with greater confidence and peace of mind.

If you believe your data privacy has been compromised, contact the following trusted sources promptly for assistance and guidance:

- Your Financial Institution (KCCU): Report suspicious activity or potential data exposure immediately so protective steps can be taken on your accounts.

- Federal Trade Commission (FTC): File an identity theft or data privacy complaint and get recovery guidance at IdentityTheft.gov.

- Credit Bureaus: Place a fraud alert or credit freeze with the major credit reporting agencies:

- Local Law Enforcement: File a police report if identity theft or financial fraud has occurred.

- Internal Revenue Service (IRS): Contact the IRS if you suspect tax-related identity theft.

Acting quickly and contacting the appropriate sources can help limit damage and protect your personal and financial information.

Safeguarding your personal and financial information requires consistent awareness and thoughtful action. By applying these practical strategies and knowing how to respond if concerns arise, you can better protect yourself from potential threats. Together with KCCU’s dedication to account security, these measures support a safer, more confident banking experience.

As the calendar turns and a new year begins, many of us set resolutions focused on health, happiness, and personal growth. This year, consider adding financial fitness to your list. According to the Pew Research Center, 40% of adults describe their current financial situation as fair, 17% as poor, and 28% expect their financial situation to worsen. Consequently, it is important to focus on developing a plan to keep your finances in check. Just like physical wellness, financial wellness is built through consistent habits, informed decisions, and the right support system. At KCCU, we believe a financially fit life helps you focus on what matters most.

What is Financial Fitness?

Financial fitness means having the knowledge, habits, and confidence to manage your money effectively. It’s about living within your means, preparing for the unexpected, and planning for your future—without constant stress. Whether you’re just starting out or refining your financial strategy, small steps can lead to big improvements.

Start with a Financial Check-Up

A new year is the perfect time to assess where you stand. Review your income, expenses, savings, and debt. Creating or updating a budget helps you see exactly where your money is going and where adjustments can be made. In return, you’ll start to feel much more in control of your finances. In the words of Dave Ramsey, “A budget is telling your money where to go instead of wondering where it went.” Think of it as your financial baseline for the year ahead.

Set Realistic, Achievable Goals

Instead of vague resolutions like “save more money,” aim for specific, measurable goals:

- Build or strengthen your emergency fund

- Pay down high-interest debt

- Save for a vacation, home, or major purchase

- Increase retirement or long-term savings

Clear goals keep you motivated and make progress easier to track.

Build Strong Financial Habits

Consistency is key to financial fitness. Automate savings, pay bills on time, and review your accounts regularly. Even small, regular contributions to savings can add up overtime. Developing these habits now can set you up for long-term success.

Use KCCU Tools and Resources

At KCCU, we’re here to support your financial journey. From savings accounts designed to help you grow your money to loans with competitive rates and personalized guidance, our team is committed to helping you make confident financial decisions. Along with our services designed to improve financial fitness, we offer a wide array of tools to help you become more knowledgeable and shape the steps you want to take next:

Financial Management & Learning Tools: KCCU partners with Zogo Finance, a gamified financial education platform that teaches money skills in bite-sized lessons. Members earn rewards like gift cards as they complete modules on topics from budgeting and saving to credit and retirement. This makes learning about money fun and rewarding.

There’s also Zogo Classroom, a platform tailored for educators to teach financial literacy to students — helping cultivate strong money habits early.

Calculators and Planning Tools: KCCU offers online financial calculators such as mortgage calculators, auto loan payment calculators, budget calculators, saving calculators, and more, that help members project outcomes and make informed decisions — for example:

- How much you’ll pay monthly on a loan

- How long it will take to pay off debt

- What your savings could grow to over time

- Mortgage and payment comparisons

These tools can help you map a path to your financial goals and better understand the impact of your choices.

Digital Banking: It’sMe247 Online Banking allows members to check balances, transfer funds, view statements, apply for loans, schedule automatic transfers, set up alerts, and much more — all from home or on the go.

The KCCU Mobile App puts full banking control in the palm of your hand. You can view account details, make mobile deposits, pay bills, transfer funds, apply for loans, and even control your debit/credit card settings.

These tools help members stay on top of their finances daily — a key part of financial fitness.

Credit Score Insights: Through SavvyMoney, KCCU members can access credit score information and educational resources to understand and monitor their credit — an important part of financial health.

Practical Support Tools: KCCU also provides forms and resources to help members efficiently manage their accounts and services — such as setting up direct deposit or automatic payments or loan payment instructions — so that transactional tasks don’t become barriers to staying financially organized.

Why This Matters for Your New Year’s Resolution

Financial fitness is more than saving; it’s about learning how to make smart financial decisions, tracking progress, and having the tools to act confidently toward your goals. KCCU’s suite of digital banking tools, educational platforms, calculators, and credit-building resources help you take control of your money and build habits that stick.

Make This the Year You Feel Financially Strong

Financial fitness isn’t about perfection, it’s about progress. This New Year, take control of your finances, one step at a time. With the right mindset and a trusted partner like KCCU by your side, you can make this your most financially fit year yet.

Ready to get started? Visit KCCU or connect with our team to learn how we can help you turn your financial goals into reality.

Kellogg Community Credit Union (KCCU) successfully concluded its annual holiday toy drive, helping ensure local children could experience the joy and excitement of the holidays. This year marked the 23rd consecutive year KCCU has proudly supported children in need through this meaningful tradition.

KCCU collaborated with the Salvation Army's Angel Tree program at its Battle Creek, Kalamazoo, and Grand Rapids branches. The Three Rivers branch and Schoolcraft branch partnered with the St. Joseph County United Way to support local foster children, while the Marshall branch worked alongside There's Enough. Thanks to the incredible generosity of KCCU members and staff, more than 800 toys were collected. These donations will make a lasting difference for many families and bring holiday cheer to children throughout the communities KCCU serves.

"The holidays are truly a magical time for children, but for many families, this season can also bring financial stress," said Tracy Miller, CEO of KCCU. "That's why this toy drive is so important to us - it allows us to come together as a credit union and as a community to help ensure every child can experience the joy and excitement of the season, while giving financial relief to those who need it most. Seeing the generosity of our members, team, and community partners year after year is incredibly heartwarming, and we are deeply grateful to everyone who helped make the holidays brighter for so many local children and families."

###

Kellogg Community Credit Union, headquartered in Battle Creek, Michigan is a full-service financial institution serving people who live, work, worship, or attend school in the state of Michigan. With $951 million in assets, KCCU proudly serves over 55,000 members in Michigan, with branches in Battle Creek, Marshall, Kalamazoo, Portage, Richland, Grand Rapids, Schoolcraft, and Three Rivers. A community leader since 1941, KCCU consistently outperforms other financial institutions with outstanding service satisfaction ratings and a long history of growth. For more information, please visit www.kccu4u.org. Connect with KCCU on Facebook, Instagram, and LinkedIn.

KCCU is proud to announce they have been honoured for the third consecutive year as one of America's Best Credit Unions in 2026 by Newsweek, placing them in the top 500 credit unions in the nation!

This award recognizes KCCU's strong community impact and commitment to their vision of "providing financial opportunity, choice, and lifelong value to our members and our community."

Newsweek, in partnership with the market research firm Plant-A Insights Group, assessed over 8,800 banks and credit unions, obtained feedback from 66,000 U.S. customers, and evaluated over 82 million online reviews. In their results, they spotlighted the top 500 credit unions in the United States on Newsweek.com, and KCCU is honored to be named on this list! Credit Unions were highlighted in their own category as being recognized that they were a financial cooperative owned by their members.

Plant-A Insights Group based their assessment on factors of the financial institution's profitability, lending activity, overall financial health and stability, operational performance, and reputation.

"We are honored and thrilled to receive the American's Best Credit Union award from Newsweek for the 3rd year in a row! This award reflects our unwavering commitment to delivering exceptional value and service to our members, so they are empowered to achieve their financial goals," said Tracy Miller, CEO of KCCU. "We are deeply grateful for the dedication of our team and the continued trust and loyalty of our outstanding members."

"More than financial service providers, credit unions are community partners, showing up in neighborhoods, participating in local initiatives and helping strengthen the connections that bind their members together," said Jennifer H. Cunningham, Editor-in-Chief of Newsweek.

You can find more detailed information on Newsweek's website, America's Best Regional Banks & Credit Unions 2026.

###

Kellogg Community Credit Union, headquartered in Battle Creek, Michigan is a full-service financial institution serving people who live, work, worship, or attend school in the state of Michigan. With $951 million in assets, KCCU proudly serves over 55,000 members in Michigan, with branches in Battle Creek, Marshall, Kalamazoo, Portage, Richland, Grand Rapids, Schoolcraft, and Three Rivers. A community leader since 1941, KCCU consistently outperforms other financial institutions with outstanding service satisfaction ratings and a long history of growth. For more information, please visit www.kccu4u.org. Connect with KCCU on Facebook, Instagram, and LinkedIn.

Throughout the winter months, you’re either saving up for holiday gifts or trying to recover from them. Financially, things might feel a bit tighter than usual, especially with ever-rising prices on just about everything. While winter gives you a good excuse to stay in and save money, it’s completely normal to feel bored and at a crossroads. Do you hibernate all winter to save cash, or do you splurge on $100 ski rentals at Boyne for one day of fun?

Luckily, KCCU is here to remind you that finding cheap winter activities in Michigan doesn’t have to be stressful. Whether you’re looking for fun with the whole family or planning something with friends, there’s plenty to enjoy during the Mitten’s snowy season.

Outdoor Activities

1. Peabody Ice Climbing - Looking for a chilling, adventurous experience that makes you feel like you’re on top of the world? Peabody Ice Climbing in Fenton, MI offers the chance to climb their 45-ft and 75-ft ice towers—perfect for both beginners and experienced climbers. It’s fun for the whole family, and day passes are $25 per person (rental gear not included).

2. Echo Valley - Get ready for a day full of excitement with Echo Valley’s snow tubing, tobogganing, and ice skating all for $25! Located in Kalamazoo, MI, you can experience sledding at a whole new level with quarter-mile toboggan runs that reach speeds of up to 60 miles per hour. If you’re looking for a longer ride, enjoy the tubing hill with a paved and heated walking path, or go ice skating throughout the park. No matter what you choose, you’re guaranteed to make warm winter memories.

3. Christkindl Market - From November 19th through December 23rd, Grand Rapids is hosting its third annual Christkindl Market. Explore a wide variety of delicious food, drinks, handmade gifts, and more, with 60+ vendors in attendance. Even if you’re not looking to buy anything, the Christkindl Market offers a warm, scenic, and festive environment to stroll through and enjoy.

4. Millennium Park - If you’re looking for an affordable place to ice skate, head to Millennium Park in Kalamazoo, MI. Admission is just $5, and skate rentals are $3. Enjoy being outdoors while taking in the city’s lively winter atmosphere.

5. Flurry of Fun - Held in Kalamazoo in February, Flurry of Fun is packed with winter activities at absolutely no cost. Enjoy a hot chocolate station, s’more station, mobile library, storytelling tent, winter golf, winter obstacle courses, snow toss, and more. It’s the perfect opportunity to bring your little ones for a magical day they won’t forget. More information on dates and pre-registration will be available in January.

6. Winter Wanderland - Downtown Battle Creek is hosting the Winter Wanderland event on December 6th from 2:00 p.m.–8:00 p.m. Explore the city while enjoying free horse-drawn wagon rides and a mini Polar Express train. You’ll also find holiday markets and artisan vendors throughout the event.

Indoor Activities